What Is the Difference Between Treasury Shares and Retired Shares? The Motley Fool

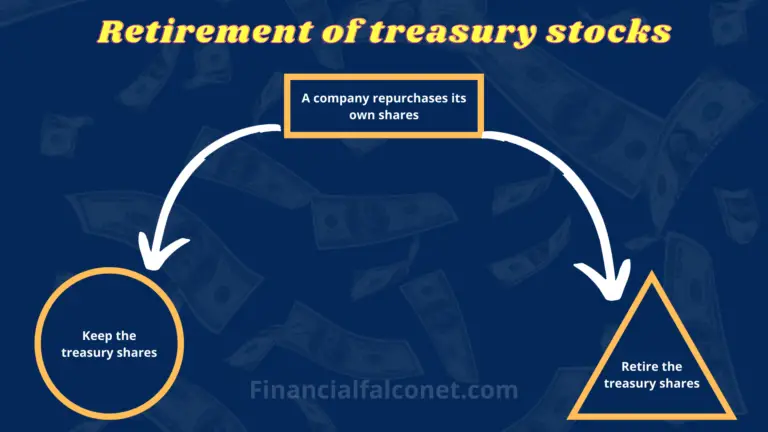

After 2 years of being in business, this company repurchased 1,000 shares at $20 per share and retired the stocks. There are two methods of journal entry for retired stocks; these are the cost method and the par value method. It’s important to point out that treasury shares still have value, and are listed on the company’s balance sheet.

After buyback

The accounting approach to the retirement of treasury stock will depend on whether the company used the par or cost method when the treasury shares were reacquired. This loss does not affect the current period’s income but reduces the credit balance in the paid-in capital account that resulted from other treasury stock transactions. Though investors may benefit from a share price increase, adding treasury stock will—at least in the short-term—actually weaken the company’s balance sheet. When a company decides to retire shares, it generally does so by issuing a notice of retirement to the shareholders. This notice states the number of shares that are being retired and the date on which they will become void.

Related AccountingTools Courses

Additionally, buying back shares can be a way for companies to return money to shareholders, and it can also help to reduce the company’s overall financial risk. If the board elects to retire the shares, the common stock and sales returns and allowances APIC would be debited, while the treasury stock account would be credited. The cost method of accounting values treasury stock according to the price the company paid to repurchase the shares, as opposed to the par value.

Shares of Stock

This arrangement essentially creates a maturity date and causes the preferred stock to act very much like a liability. First, listed companies must report and announce the information of share repurchase to the FSC by the ‘Regulations on Share Repurchase by Listed Companies‘ and input it into the Market Observation Post System (MOPS). Among this information, the cost of the repurchase should be determined by the FSC. On the balance sheet, treasury stock is listed under shareholders’ equity as a negative number. These shares are issued by the company to the public and provide shareholders with ownership in the company, voting rights on corporate matters, and eligibility to receive dividends.

- The number available only to the public to buy and sell is known as the float.

- The remaining $1,500 difference of the $4,500 economic loss is charged to Paid-in Capital From Sale of Common Stock Above Par.

- Canceled shares are different from treasury shares (also known as treasury stocks).

- When a company buys back its shares, they are recorded in its account and can be converted to preferred shares or bonds at any time.

- In short, while common stock represents ownership and active participation in the company, treasury stock is a strategic tool companies use to manage their capital structure and shareholder value.

Journal Entry for Retiring Treasury Stock

In the United States, the Securities and Exchange Commission (SEC) governs buybacks. These shares can benefit existing shareholders by increasing their ownership stake in the company and improving financial metrics like earnings per share. It may also positively impact the stock price due to the reduced number of shares available in the market. Retired shares refer to shares of a company’s stock that have been repurchased or redeemed by the company and are no longer outstanding or held by shareholders. Nevertheless, investors may fear future shares dilution if a business has large unsold and authorized shares.

Treasury Stock Cost Method vs. Par Value Method

Our team of reviewers are established professionals with decades of experience in areas of personal finance and hold many advanced degrees and certifications. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own.

Some states in the United States have specific laws on how to account for retired stocks and therefore, may differ from what is stated here. The reasons for crediting Additional Paid-in Capital and debiting Retained Earnings are the same as for retirements of newly acquired shares. In each case, both the Common Stock account and the Paid-in Capital from Issue of Common Stock in Excess of Par account are debited for the amounts per share for which they were originally credited. In order to make the callable shares marketable, the corporation typically agrees to pay (at the time of call) not only par value but also an amount in excess of par known as the call premium. Callable stock (virtually always preferred shares) gives the corporation the right to buy the stock from the owner according to a prearranged schedule of prices and times. If the original issue price exceeds the amount paid, the remaining credit should be recorded in the Additional Paid-in Capital account.

As a result, when creditors require restrictions on dividend payments, they also often require restrictions on treasury stock purchases. This process of going private is often accomplished through treasury stock purchases because corporate funds are used instead of the personal resources of the surviving stockholders. If this is management’s goal, it can choose to keep the treasury stock on its books—perhaps hoping to sell it later at a higher price—or simply retire it. However, in certain situations, the organization may benefit from limiting outside ownership. Reacquiring stock also helps raise the share price, providing investors with an immediate reward. Under the TSM, the options currently “in-the-money” (i.e. profitable to exercise as the strike price is greater than the current share price) are assumed to be exercised by the holders.

When the organization undergoes a public stock offering, it will often put fewer than the fully authorized number of shares on the auction block. That’s because the company may want to have shares in reserve so it can raise additional capital down the road. The cash account is credited for the amount paid to purchase the treasury stock. Following the repurchase, the formerly outstanding shares are no longer available to be traded in the markets and the number of shares outstanding decreases – i.e. the reduced number of shares publicly traded is referred to as a decline in the “float”. Retired shares Sometimes when a company buys back shares of its own stock, it doesn’t have the desire to hang on to them. In this case, the company can choose to cancel, or retire the shares according to SEC regulations.

Treasury stocks (also known as treasury shares) are the portion of shares that a company keeps in its own treasury. They may have either come from a part of the float and shares outstanding before being repurchased by the company or may have never been issued to the public at all. On the shareholders’ equity section of the balance sheet, the “Treasury Stock” line item refers to shares that were issued in the past but were later repurchased by the company in a share buyback. Similarities Treasury shares and retired shares have a few things in common. Most notably, neither type is included when calculating the company’s number of outstanding shares.

Commenti recenti